Life Insurance Retirement Plans: Turning LIRPs into Powerful Retirement Tools

Let’s face it: when most people think of either life insurance or retirement planning, “exciting” isn't the first word that comes to mind.

But when those terms are combined into a “Life Insurance Retirement Plan,” the mundane concept turns into a crafty strategy that could give you access to sizable loans you might not even need to pay back while you’re still alive.

The Life Insurance Retirement Plan (LIRP) is a financial tool that combines the benefits of life insurance with the growth potential and tax advantages typically associated with retirement accounts.

In this LIRP guide, we'll explore how high-earners can use LIRPs to keep more of what they’ve earned and learn about a few extra benefits.

What is a Life Insurance Retirement Plan (LIRP)?

A LIRP leverages permanent life insurance policies to provide retirement income.

Unlike term life insurance, which offers coverage for a specific period, permanent life insurance policies build cash value over time, which can be accessed during retirement.

Your cash value in a LIRP grows tax-deferred, and if structured correctly, withdrawals can be made tax-free.

The permanent life insurance umbrella category covers three distinct types of insurance:

- Whole life insurance offers fixed premiums, a guaranteed cash value, and a death benefit. It provides the most stability but may have lower growth potential than other types.

- Universal life insurance offers flexible premiums and death benefits. The cash value grows based on a fixed interest rate set by the insurer. It provides more flexibility but can be more complex to manage.

- Indexed universal life insurance (IUL) is similar to universal life but ties the cash value growth to a stock market index like the S&P 500. This offers higher growth potential but comes with more risk.

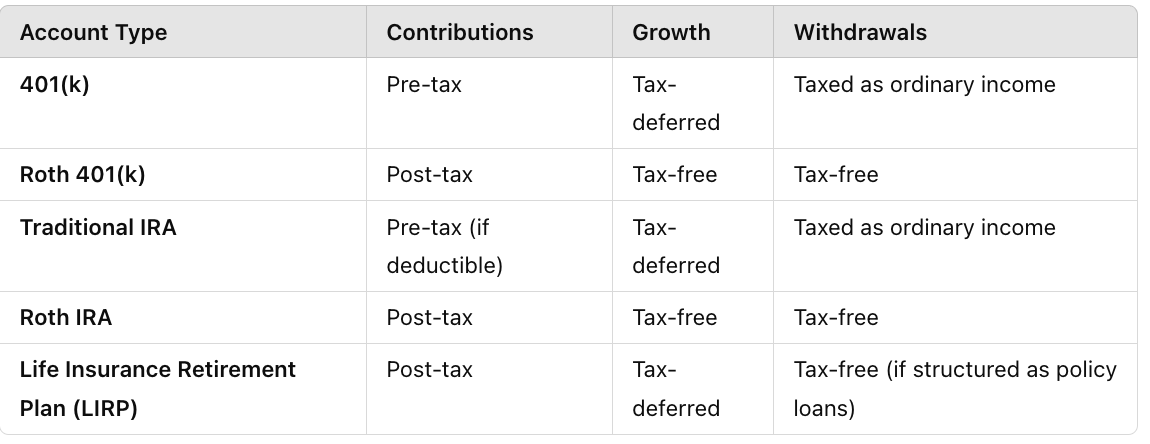

How Do LIRPs Compare to Traditional Retirement Accounts?

Contribution Limits

🥇 LIRPs don’t have contribution limits, making them attractive for folks who want to save more.

🥈401(k) and IRA contributions are capped annually; for 2024, the 401(k) limit is $23,000 (plus $7,500 catch-up if over 50), and the IRA limit is $7,000 (plus $1,000 catch-up if over 50).

Tax-Deductible

🥈LIRP contributions (premiums) aren’t tax-deductible, and you can’t reduce your taxable income by the amount of your contributions, unlike contributions to traditional IRAs or 401(k) plans. LIRPs offer tax-deferred growth and potentially tax-free withdrawals if structured properly– we’ll get into this later.

🥇Contributions to 401(k)s and traditional IRAs are tax-deductible, and the funds grow tax-deferred. Withdrawals are taxed as ordinary income. Roth IRAs offer tax-free withdrawals but have income and contribution limits.

Withdrawal Flexibility

🥇 LIRPs do not have RMDs, providing more flexibility in accessing funds.

🥈 Traditional retirement accounts have required minimum distributions (RMDs) starting at age 72.

Additional Considerations:

LIRPs include a death benefit, which can provide additional financial security for your beneficiaries.

So, you essentially get some of the most significant benefits of retirement accounts with a significant lump sum that can be paid to your loved ones in the unlikely and unfortunate scenario of your passing.

How LIRP Tax-Free Withdrawals Work

As noted above, you contribute after-tax dollars to your permanent life insurance policy through premiums, and the cash value within a grows tax-deferred. If you were to access your growth, you’d pay taxes on it as ordinary income. However, policy loans (more on below) allow you to avoid that entirely.

Part of your premiums pay for the life insurance aspect, and part grows within the account.

So, as the cash value accumulates over the years, you don’t pay tax on the growth, similar to the tax-deferred growth in traditional retirement accounts like IRAs and 401(k)s.

LIRPs allow you to access the accumulated cash value to provide a retirement income stream through a mix of policy loans and withdrawals.

Policy Loans

You can borrow against the cash value of your life insurance policy.

These loans aren’t considered taxable income because they are technically loans that must be repaid and usually come with favorable interest rates compared to other borrowing options.

Withdrawals

Direct withdrawals from the cash value are tax-free up to the amount of premiums paid.

Your profit (amount withdrawn beyond the premiums) is taxable as ordinary income.

How to Structure a LIRP Correctly

Plan to avoid direct withdrawals as a first resort since the amount exceeds the total premiums paid into the policy.

Instead, you can give yourself a hearty cash injection without any tax implications by taking policy loans.

While it’s possible to repay these loans, many policyholders plan to keep the loan outstanding until death.

The death benefit is then used to pay off the loan balance, and the remaining amount is tax-free to the beneficiaries.

However, if the loan balance gets too high relative to the cash value, the policy could lapse, leading to a significant tax liability. Make sure you work with a financial planner to ensure the loan balance doesn't get too high relative to cash value.

Here’s how that doozie of a situation plays out:

When a life insurance policy lapses, the outstanding loan balance is treated as if it were distributed to the policyholder. This means the IRS considers it previously tax-deferred income and now requires it to be reported as taxable income.

The taxable amount is the difference between the total loan balance and the policyholder's basis in the policy (the total amount of premiums paid into the policy).

Since the outstanding loan is now considered taxable income, it can push the policyholder into a higher tax bracket, resulting in a substantial tax bill.

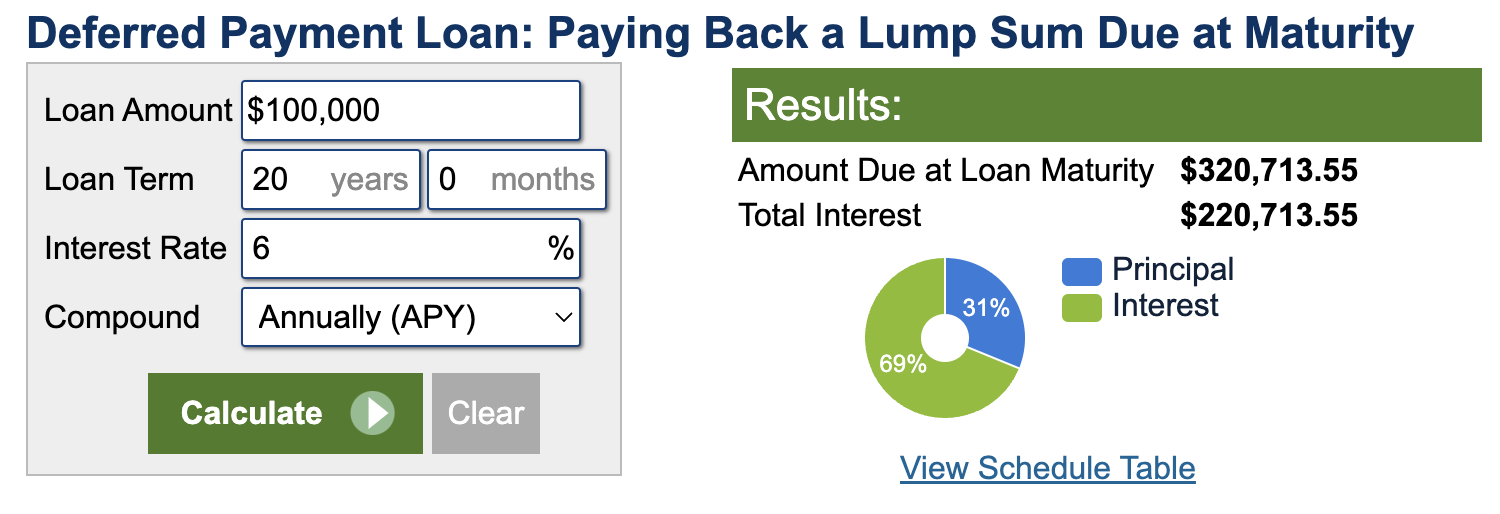

A LIRP in Motion: A Practical Example

Richard has a life insurance policy with a significant cash value. He paid $200,000 in premiums over several years, and his cash value has grown to $500,000. His death benefit is $1,000,000.

Richard takes a policy loan of $100,000 at 6% APY compounded annually. The loan isn’t taxed as income.

If Richard decides not to repay the loan or the interest during his lifetime, the outstanding loan balance and its interest will be deducted from the death benefit of $1,000,000.

Let’s assume Richard meets his maker in 20 years. His total amount due would be $320,713.55, $220,713.55, which would be the total interest accumulated over the loan’s duration.

All of this would be deducted from his net death benefit, leaving his beneficiaries $679,286.45 tax-free.

Alternatively, Richard could pay the interest regularly and prevent the loan balance from increasing exponentially, which reduces the risk of the policy lapsing due to a ballooning loan balance.

Policy Lapses and How to Prevent Them

A policy lapse occurs when the cash value is insufficient to cover the policy’s costs and the outstanding loan balance.

Here’s how this could happen:

As the interest on Richard’s loan accrues annually at 6%, it compounds and increases the loan balance significantly over time. If the interest is not paid, it is added to the loan principal, causing the debt to grow.

His policy has ongoing costs, including the cost of insurance and administrative fees; if he stops paying them out of pocket, these costs would be deducted from the cash value, reducing the available balance.

If Richard continuously avoids paying the interest, the increasing loan balance and policy costs will deplete the cash value.

Once the cash value is exhausted, the policy may lapse, and the insurance company will terminate it and use the remaining cash flow to cover the expenses.

Preventing Policy Lapses

To prevent unintentional policy lapses, you should make regular interest payments out-of-pocket, continue paying premiums to support the policy’s costs to avoid your cash balance from decreasing and keep an eye on the policy’s cash value and loan balance to ensure the policy remains sustainable.

Tailoring your policy to your anticipated needs from the get-go can make all the difference.

For example, some policies offer fixed annual payments, which are easier to account for but may hinder growth, whereas others are tied to the stock market, which may go up more but also present the risk of a downside.

Caught on the lousy end of mounting interest payments and a decreasing cash balance, a policy lapse could result.

Also, make sure your plan offers flexible repayment options, such as repaying the loan or using the death benefit to cover the outstanding balance.

A financial planner can help you spell out all the potential nuances you want to account for.

Making Cents of LIRPS

A thought-out LIRP strategy can provide a significant, tax-free surge of cash during retirement, supplementing other retirement accounts.

LIRPs shine bright when you consider that the policy loans aren’t considered income.

On one hand, if your cash balance in your LIRP has appreciated significantly, you could take out a hefty loan that allows you to coast through retirement, resting easy on your calculations that your repayment will come from your death benefit.

On the other hand, you can repay the interest as you would any other loan using funds from, let’s say, your traditional retirement accounts and keep the death benefit entirely intact for your beneficiaries.

As we wrap up our discussion on Life Insurance Retirement Plans (LIRPs), let’s distill the key advantages and drawbacks.

LIRP perks include tax-free distributions (if structured as policy loans), a tax-free death benefit for your beneficiaries, often a guaranteed interest rate (depending on the provider and plan), growth potential, and accelerated benefit riders (that allow for death benefit access in case of qualifying events like terminal illness), and special provisions.

The top of the list of LIRP cons includes that your contributions are non-deductible, unlike contributions to traditional retirement accounts, and that LIRPs tend to be higher due to the insurance benefits you’re paying for. Further, the guaranteed interest rates may be lower than other investment options, and your options may be more limited than other retirement savings vehicles.

Still, LIRPs are a powerful tool to consider. No other retirement savings accounts include the added benefit of disbursing a large lump sum of cash to your loved ones as a death benefit. However, they’re still handy for those of us who want to maximize our benefits during our time on this Earth, allowing us to tap into loans we don’t even have to pay back while we’re still alive (in most cases.)

Discussing how LIRPs fit into your broader retirement picture with a financial planner can help you determine whether they meet your current and future needs.